.svg)

Synthetic Identity Fraud Renters: What Property Managers Need to Know and Do

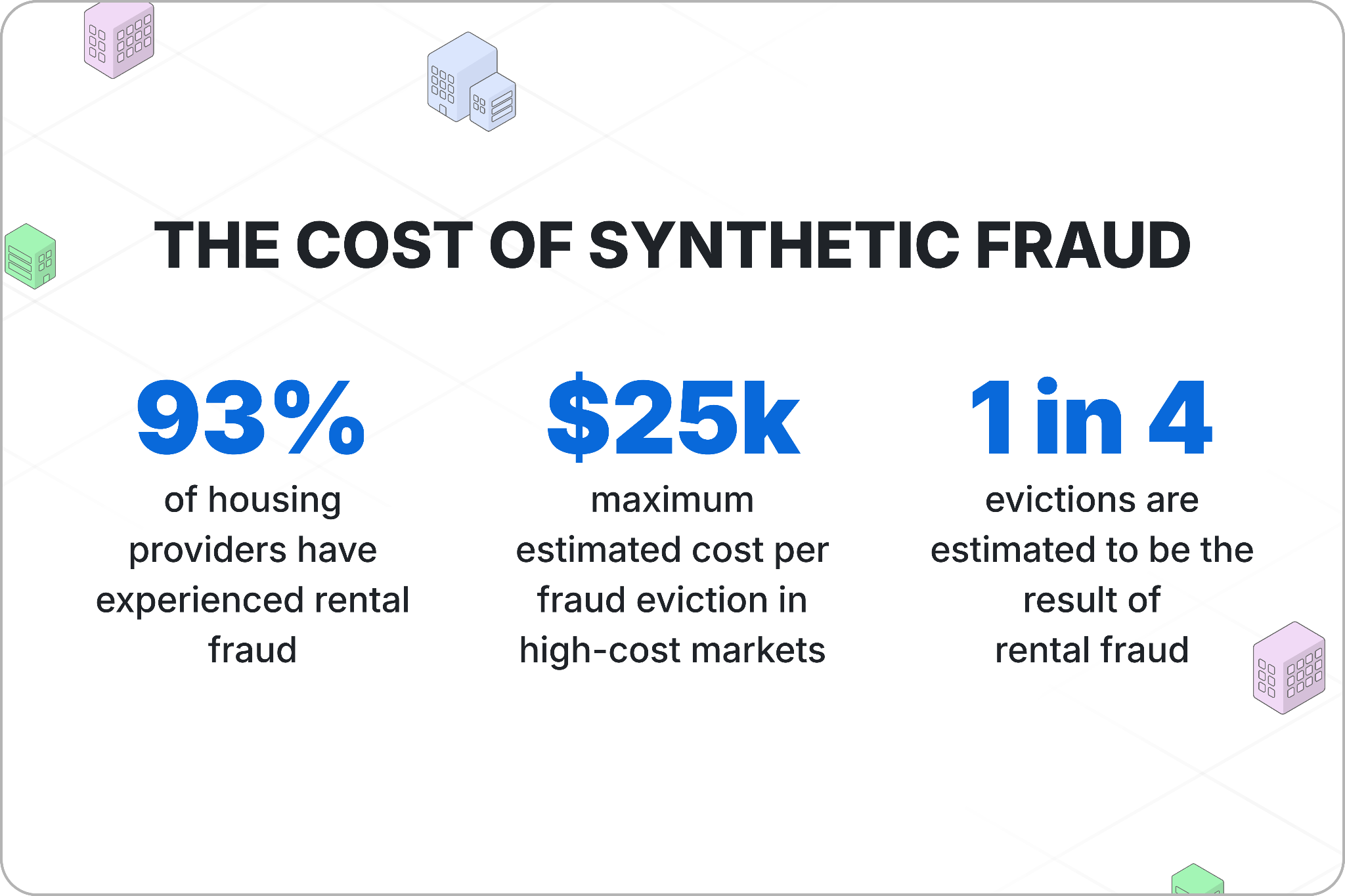

Synthetic identity fraud renters are no longer a fringe concern in multifamily housing. According to the National Multifamily Housing Council, 93% of housing providers have reported experiencing rental fraud, and synthetic identity fraud is now the fastest-growing type of fraud in the industry.

Unlike traditional identity theft, synthetic fraud creates applicants who technically do not exist, making it far harder to detect and far more expensive to resolve.

This post explains what synthetic identity fraud is, why it is accelerating, what it costs property managers, how to spot it, how to stop it, and what to do when you find it.

What Is Synthetic Identity Fraud?

Synthetic identity fraud is when a fraudster combines real data, typically a stolen Social Security number belonging to a child, elderly person, or deceased individual, with fabricated information such as a fictitious name, birthdate, and address, to construct a persona that does not actually exist.

Because no single real person is being fully impersonated, there is no obvious victim to raise an alarm. The fabricated identity can build a functional credit history over months or years, making it appear legitimate to standard screening tools.

Synthetic Identity Fraud vs. Traditional Identity Theft

Traditional identity theft falls into two categories:

- First-party fraud is when an applicant misrepresents their own history: inflating income, hiding evictions, or lying about employment.

- Third-party fraud is when a fraudster steals a real, living person's complete identity and applies as that individual.

In both cases, a real person exists and can eventually discover the crime and dispute it.

Synthetic fraud is different. The constructed persona is not tied to any single victim who will notice unauthorized accounts or flag suspicious activity.

By the time a property manager discovers the fraud, the renter may have disappeared entirely, leaving behind unpaid rent, legal costs, and no one to pursue.

How Synthetic Identities Are Built

The foundation is almost always a stolen Social Security number. Fraudsters target SSNs belonging to children (who have no established credit history), elderly individuals, or people who have recently died. These numbers are purchasable on dark web markets at low cost, a direct consequence of large-scale data breaches.

Some fraudsters use Credit Privacy Numbers (CPNs) instead. CPNs are marketed online as tools to "restore your credit" or "start fresh," but they are either fabricated nine-digit numbers or stolen SSNs repackaged and sold under a different label. Purchasing a CPN is itself illegal under federal law.

Once the number is in hand, the fraudster spends months building a thin but passable credit profile: opening secured cards, becoming an authorized user on existing accounts, and making small on-time payments.

By the time they submit a rental application, the synthetic persona has a functioning credit score that passes a basic pull.

Why Synthetic Identity Fraud Is Surging in Rental Housing

Data Breaches Have Put Real SSNs Within Easy Reach

Building a synthetic identity requires one real ingredient: a genuine Social Security number. Data breaches have made that ingredient far easier and cheaper to obtain than it has ever been.

US data breaches increased by 15% year over year in 2023, and the average breach risk severity, defined as the ability of a breach to enable downstream identity fraud, reached its highest recorded level that same year, according to TransUnion data cited by Findigs.

The practical result is that fraudsters can now acquire a real SSN cheaply, attach fabricated personal details to it, and begin building a synthetic credit profile with minimal upfront cost or technical skill.

Digital Leasing Removed the In-Person Check

The broad shift to remote and online leasing workflows eliminated the natural friction that in-person meetings provided. Leasing agents previously had a chance to observe whether the person standing in front of them matched the documents being submitted.

That opportunity is largely gone in a fully digital application process.

Fraudsters now submit polished applications remotely, often refusing live video calls or offering vague excuses when asked to verify their identity in real time. The absence of physical interaction is precisely what makes synthetic fraud viable at scale.

Organized Fraud Networks and Template Farms

Synthetic identity fraud in rental housing is not primarily the work of lone actors.

Criminal organizations known as template farms mass-produce fake pay stubs, bank statements, employment verification letters, and ID documents. These materials are sold as packages and increasingly promoted through social media platforms, including TikTok and Instagram, where fraud kits are advertised with step-by-step tutorials.

Property management teams are not contending with occasional opportunists. They are contending with repeat, coordinated operations that test and refine their methods across many applications at many properties simultaneously.

The Cost of Synthetic Identity Fraud for Property Managers

Direct Financial Losses

When a synthetic identity renter stops paying rent, property managers are pursuing a person who does not legally exist. There is no credit to garnish, no employer to contact, no real address to serve.

The average cost of a fraud-related eviction can reach $25,000 when accounting for unpaid rent, legal fees, property damage, and unit turnover, and roughly one in four evictions nationwide stems from rental fraud (NMHC, 2024).

Safety and Community Risk

Synthetic applicants bypass criminal background checks entirely because the identity being checked has no criminal record. Property managers who rely on background screening as a safety mechanism have no way to know who actually moved into the unit.

Some fraudsters use synthetic identities to secure multiple apartments simultaneously, then run illegal subletting operations out of those units before disappearing. This creates safety and liability exposure for the property, neighboring residents, and the management team.

Warning Signs in Rental Applications

The following signals warrant a closer look. They are not automatic grounds for denial, but should trigger additional verification steps before a decision is made.

a

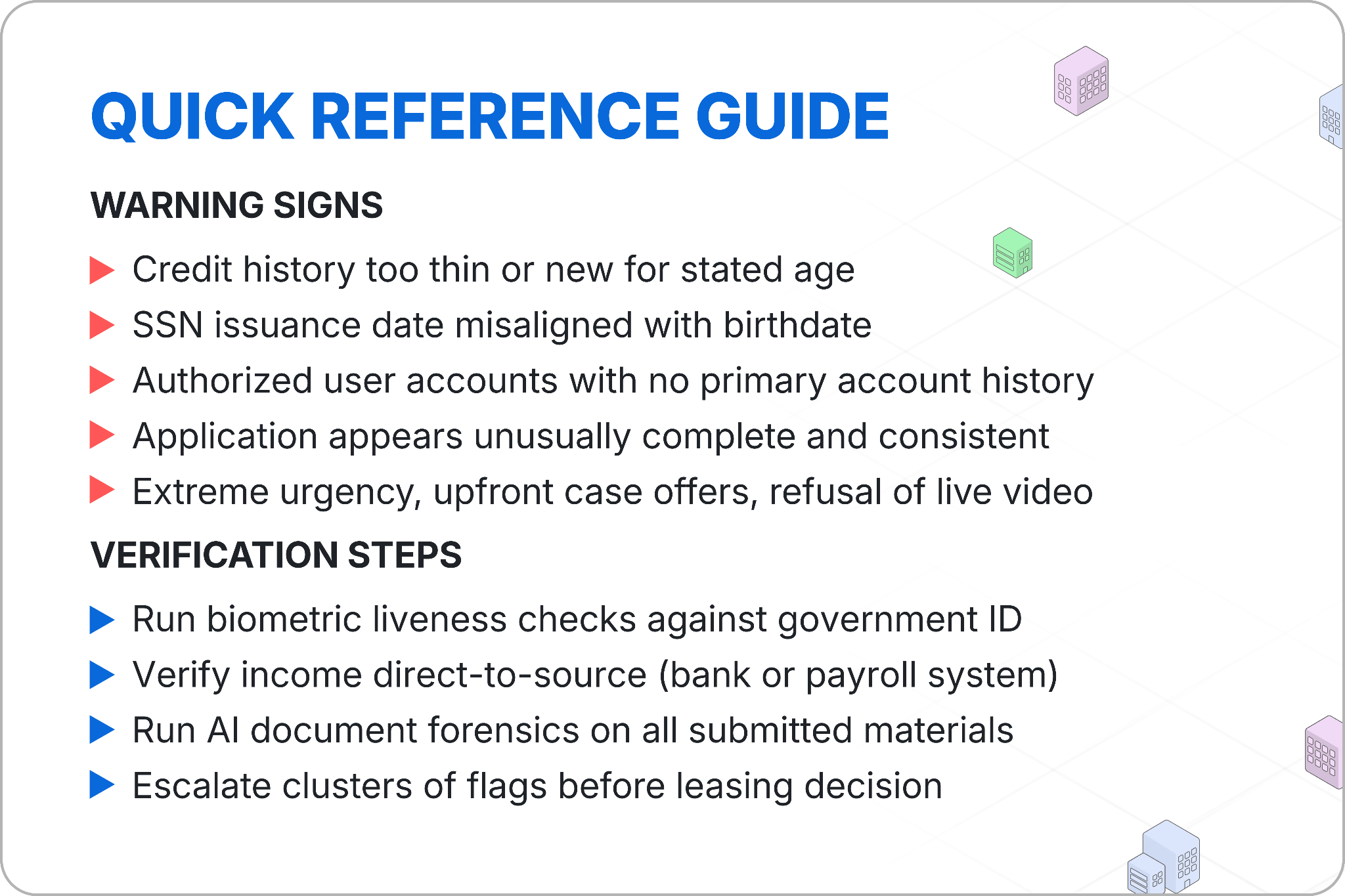

A credit history that appears too thin or too new relative to the applicant's stated age is one of the clearest signals. A 35-year-old with two years of credit history and no derogatory marks is worth a second look.

Specific anomalies to watch for include:

- An SSN issuance date that does not align logically with the provided birthdate.

- Authorized user accounts with no accompanying primary account history, a tactic used to inflate a synthetic identity's score quickly.

Application and Behavioral Red Flags

Ironically, applications submitted by synthetic identity fraud renters can appear unusually complete and consistent. Genuine applications almost always contain small natural inconsistencies. A file that looks perfectly assembled across every document type is a signal, not a green light.

Behavioral signals matter equally. Watch for extreme urgency to sign quickly, offers to pay multiple months of rent upfront in cash, reluctance to participate in a live video call, and mismatched details across documents that each appear individually legitimate.

Any one of these alone is not disqualifying. A cluster of them warrants escalation.

How to Stop Synthetic Identity Fraud Renters

Move Beyond Standard Credit Checks

Standard credit checks were built to verify that an SSN has a credit history attached to it. They were not built to confirm whether the person submitting an application is the true owner of that SSN.

A synthetic identity with a cultivated credit profile will pass a basic credit pull without triggering a flag. Manual document review is equally insufficient against AI-generated pay stubs and bank statements that replicate genuine formatting at the pixel level.

Implement Multi-Layered Identity and Income Verification

Effective prevention requires layered controls working together. No single tool closes every gap on its own.

Biometric liveness checks require applicants to submit a live selfie matched against a government-issued ID in real time. A synthetic identity has no real face to match against forged documents. This single step eliminates a large proportion of synthetic fraud attempts before they advance.

Direct-to-source income verification bypasses applicant-provided documents entirely by connecting directly to the applicant's bank account or payroll system via platforms such as Plaid. This removes the opportunity to submit fabricated statements.

AI-powered document forensics analyzes metadata, formatting patterns, and behavioral signals across submitted documents to flag anomalies that human reviewers consistently miss. Properties that implement this layer report significantly reduced fraud rates at the application stage.

Some property managers also work with rent guarantor services as part of their screening stack. When a renter applies with guarantor backing, they have already been underwritten through a separate qualification process, which means a synthetic identity would need to clear two independent sets of checks rather than one.

It is not a substitute for the verification steps above, but as one additional layer in a larger system, it adds meaningful friction at the right point in the pipeline.

Train Your Leasing Team

Technology is one layer. The leasing team is another. Staff should be trained to recognize behavioral red flags during initial contact:

- Urgency to bypass the standard process.

- Reluctance to appear on a live call.

- inconsistent verbal responses when asked follow-up questions about application details.

Establish a documented internal escalation protocol so staff know exactly when and how to flag a suspicious application before a leasing decision is made. A clear process removes ambiguity and ensures that borderline cases get a second review rather than slipping through on urgency alone.

What to Do When You Suspect Synthetic Identity Fraud

Traditional background checks verify consistency across documents. They were designed to confirm that information matches across sources, not to confirm whether the combination of information represents a real person.

A synthetic identity built over months will pass a consistency check because the fraudster has made sure all the pieces align. This is why detection requires going beyond the documents themselves.

Document Everything First

Before taking any action on a suspected synthetic fraud application, compile all application materials, communications, and the specific inconsistencies that triggered concern.

Thorough documentation protects the property owner in any subsequent legal proceeding and supports a defensible adverse action if the application is denied.

Adverse Action and Denial Letters

If an application is denied based on information from a consumer reporting agency, federal law under the Fair Credit Reporting Act requires an adverse action notice. The notice must identify the consumer reporting agency used, inform the applicant of their right to obtain a free copy of the report, and explain their right to dispute inaccurate information.

This requirement applies regardless of whether the denial is fraud-related. Failure to issue a compliant adverse action notice creates legal exposure independent of the fraud itself.

When to Escalate to Legal Counsel or Law Enforcement

If a synthetic identity renter is already occupying a unit, the eviction process must follow standard legal procedure in that jurisdiction regardless of the fraud. There are no shortcuts. Involve legal counsel early to avoid procedural missteps that extend the timeline and increase costs.

If the fraud involves a stolen SSN belonging to a real person, there may be grounds to report to law enforcement or the Federal Trade Commission.

Reporting also creates a record that can be useful if the same synthetic identity appears at another property. Specific processes and obligations vary by state.

Conclusion

Synthetic identity fraud is an industrialized threat. The fraudsters behind it are organized, technically sophisticated, and experienced at exploiting the gaps in standard screening workflows.

No single tool eliminates the risk entirely, but a layered approach combining biometric verification, direct-to-source income confirmation, AI document forensics, trained leasing staff, and clear post-detection protocols dramatically reduces exposure at the application stage.

Working with a rent guarantor service like Cosign adds one more independent check to that stack. Applicants who arrive with Cosign backing have already been underwritten through a separate qualification process, which means a synthetic identity would need to clear two independent reviews rather than one.

The cost of building a stronger screening process is predictable. The cost of a synthetic fraud eviction is not.

.avif)

.avif)

Let’s boost your occupancy rates