.svg)

Does Paying Rent Build Credit? A Complete Guide for Renters

For most renters, monthly rent is the biggest check they write. But unless someone is actively reporting those payments, they count for nothing on a credit report. Rent does not automatically build credit.

The good news: with the right setup, it absolutely can. This guide covers how rent reporting works, which services are worth considering, what it costs, and how to avoid the pitfalls that can actually hurt your score instead of helping it.

If you are working toward qualifying for your next apartment, building a stronger credit profile is one of the most useful things you can do right now.

Does Paying Rent Automatically Build Credit?

No. Rent is a cash-like transaction, not a credit account. Unlike a car loan or a credit card, your lease agreement does not get reported to any credit bureau by default. Your landlord has no automatic obligation to share your payment history with Experian, TransUnion, or Equifax, and most do not.

All three major credit bureaus will include rent data on your credit report if they receive it from a verified source. The key phrase there is "if they receive it." That data has to be sent by someone, either your landlord through a reporting platform or you through a third-party service.

Does Applying for an Apartment Affect Your Credit?

Whether applying for an apartment affects your credit depends on how the landlord screens you.

Most landlords and property managers use soft inquiries when checking your credit as part of a rental application. Soft inquiries do not affect your credit score at all. Some landlords, particularly those using certain third-party screening services, may run a hard inquiry instead, which can cause a small, temporary dip of a few points.

Before you apply, it is worth asking your landlord which type of pull they use. If you use Cosign, the screening is always a soft pull and will not impact your score.

How Does Rent Reporting Build Credit?

The Role of Credit Bureaus in Rent Reporting

When rent payments are reported to one or more of the three major bureaus, they are added to your payment history. Payment history is the most heavily weighted factor in most credit scoring models, accounting for a significant portion of how your score is calculated. Consistent, on-time payments reported over months and years signal to lenders that you are a reliable borrower.

The catch is that someone has to send that data. Either your landlord uses a platform that submits it automatically, or you sign up with a third-party service that verifies and reports it on your behalf.

Which Credit Scoring Models Count Rent Payments?

Not all of them. VantageScore 3.0, VantageScore 4.0, and FICO Score 9 all factor in reported rent payments when calculating your score. If your payments are being reported, these models will reflect them.

However, not every lender or landlord uses the same scoring model, so the impact of rent reporting on the specific score they pull may vary.

On-Time Payments vs. Late Rent: What Gets Reported

On-time rent payments, when reported, strengthen your payment history the same way a credit card payment would. Over time, a consistent record of on-time rent adds positive history to your file.

Late or missed rent can cause damage through two separate pathways.

First, if your landlord uses a reporting service that submits all payment data (not just positive payments), a late payment can be reported directly to the bureaus.

Second, if unpaid rent is sent to a collections agency, that collection account will appear on your credit report regardless of whether any reporting service was in place. A collection account can stay on your report for up to seven years.

Before enrolling in any rent-reporting service, confirm whether it reports only positive data or all data. That one distinction can be the difference between a helpful tool and a liability.

How to Report Rent Payments to Credit Bureaus

Reporting your rent is more straightforward than it might sound. Here is how to approach it in two steps.

Step 1: Check Whether Your Landlord Already Reports

Before signing up for anything, ask your landlord or property manager whether they already use a rent-reporting platform. Services like Esusu, RentTrack, and PayYourRent are built for landlords and property managers, and if your building is already enrolled, you may be able to opt in at no cost to you.

This is the easiest path. One conversation can save you a monthly fee and get your payments reporting to the bureaus starting with your next rent cycle.

Step 2: Choose a Service and Enroll

If your landlord does not report, you can set up reporting yourself through a third-party service. The general enrollment process works like this:

- You provide proof of your lease, your payment records, and your landlord's contact information.

- The service verifies your rental history and begins reporting your payments to one or more credit bureaus.

Some services route rent payments through their platform before forwarding them to your landlord. Others verify your payments independently without changing how you pay. Check the mechanics before you enroll so you know exactly what you are signing up for.

Free Ways to Report Rent to Credit Bureaus

If cost is a concern, Experian Boost is the most widely available free option. It connects to your bank account, identifies qualifying on-time rent and utility payments, and adds them directly to your Experian credit file at no charge.

There's a caveat, though: Experian Boost only reports to Experian, not to TransUnion or Equifax. If a lender or landlord pulls your credit from one of the other two bureaus, they will not see your rent history.

For renters who want all three bureaus updated, a paid service is the only current option.

Paid Rent-Reporting Services

Several subscription-based services report to all three major bureaus.

Boom reports to all three and is designed to submit only positive payment data, which reduces the risk of a late payment causing damage.

Services like Self, Piñata, and RentReporters offer similar functionality and many allow you to back-report up to 24 months of past rental history for an additional fee, which can give your credit file an immediate boost if your payment record has been strong.

Fees vary across services, including setup fees, monthly subscription fees, and back-reporting fees. Before enrolling, confirm which bureaus the service reports to, whether it reports positive data only or all data, and what the total cost will be.

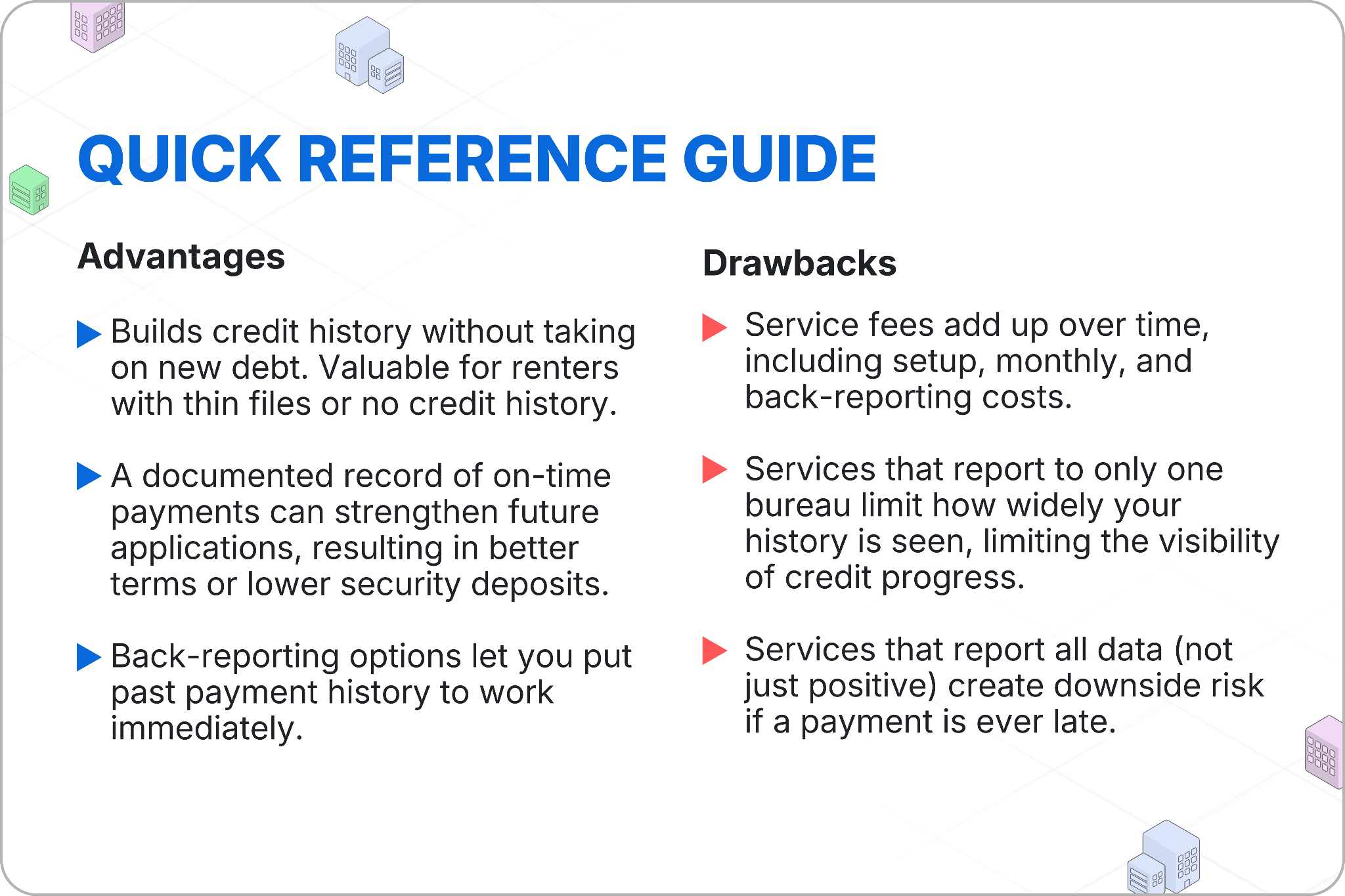

Pros and Cons of Using Rent to Build Credit

Other Ways to Build Credit While Renting

Pay Rent With a Credit Card

Some property managers accept credit card payments for rent. If yours does, paying rent with a card and paying the balance in full each month builds payment history and can earn cash-back or travel rewards on a large recurring expense.

Two risks to watch:

- Most property managers charge a convenience fee of around 2.5% to 3% for credit card payments, which can offset the value of any rewards.

- Charging a large amount to your card raises your credit utilization ratio. If you carry that balance rather than paying it off, the interest charges and the utilization hit can do more damage than the credit-building benefit is worth.

Secured Credit Card or Credit-Builder Loan

Both options work independently of your landlord and are well-suited for renters who are just starting to build credit.

A secured credit card requires a refundable deposit, typically equal to your credit limit, and reports your payments to the bureaus like any other credit card.

A credit-builder loan holds funds in an account while you make fixed monthly payments, and the payment history is reported throughout the loan term.

Become an Authorized User

If a trusted family member or friend has a credit card with a long, positive history, being added as an authorized user can extend some of that history to your credit file.

You do not need to use the card or even hold it physically. The account activity shows up on your report and can strengthen your file without requiring you to take on any financial risk directly.

Report Utility Bills

Utility payments (electricity, phone, internet, water) are not automatically reported any more than rent is, but tools like Experian Boost and eCredable can add them to your credit report using the same logic as rent reporting. If you are already setting up rent reporting, adding utilities at the same time is a low-effort way to generate additional positive history.

How Much Will My Credit Score Increase From Rent Reporting?

It depends heavily on where your credit file stands today.

Renters with thin files or no credit history at all tend to see the largest gains from rent reporting, sometimes 50 to 100 points, because adding any positive payment history to a sparse file has an outsized effect.

Renters with established credit profiles and a mix of accounts may see a smaller lift, since their scores are already shaped by a range of factors.

The most consistent factor in any credit improvement is time. Rent reporting works best as a long-term habit rather than a quick fix. The longer your record of on-time payments, the more weight it carries.

The Bottom Line

Paying rent does not automatically build credit, but it can. The difference is whether someone is reporting those payments to the credit bureaus.

Start by asking your landlord whether they already use a reporting platform. If they do not, compare third-party services on bureau coverage, reporting type (positive only vs. all data), and total cost before enrolling.

And above all, prioritize on-time payments. Reporting gives your rent the chance to help your score. On-time payments are what actually do the work.

If you are building credit specifically because you want to qualify for your next apartment, Cosign is one tool designed for exactly that situation. Cosignis a third-pparty guarantor service that helps renters qualify even when they narrowly miss standard income or credit thresholds. We show you how it works and compare the top guarantor services in this article.

.avif)

.avif)

Aumentemos tus tasas de ocupación